Industry News

Mixed signals on container freight rates as Red Sea alarm subsides - Seatrade Maritime

Linerlytica, however, reported this week that “the stage for a series of larger rate hikes in May” has been set by the third straight increase in the Shanghai Container Freight Index (SCFI).

“Capacity utilisation is tightening across all main trades on stronger market demand, which will aid carriers’ GRI [general rate increase] efforts,” said the analyst.

Dynamar reports a confusing rate scene with the Ningbo Containerized Freight Index (NCFI) showing a decline since Chinese New Year.

“Rates were in slight positive territory before the Lunar New Year but have come under pressure since then with the overall index -13% on its year-start position come mid-April,” said Dynamar analyst Darron Wadey.

“For individual trades there were significant differences though, with Europe/Mediterranean indices averaging -23% whilst intra-Asia equivalents were +22% up, on average,” he added.

Meanwhile, the China Containerized Freight Index (CCFI), which Dynamar says is “more than spot rates, is usually less volatile than other indices, was around 60% up for February, but it too has calmed down to +30% up two months later, according to Wadey.

“So, a similar pattern to the NCFI of growth and fall back, it’s just that the severities are different. Here though, the Europe/Mediterranean trades were +54% up on the year start (average of two) whilst intra-Asia routes were only marginally better (also average of two), In other words, the opposite of the NCFI experience,” explained Wadey.

Drewry’s World Composite Index (WCI) is more in line with the NCFI and CCFI indices, with analyst Simon Heaney telling Seatrade Maritime News that the index has been on a “12-week skid”.

“The WCI has been declining week-on-week since early February,” said Heaney, “Average rate declines were $94 per 40ft in February, that accelerated to $141 per 40ft in March but the rate of decline has again eased to an average of $70 per 40ft this month.”

Drewry and Linerlytica diverge significantly over the transpacific contract rates currently under negotiation. Linerlytica claims contracts “are settling 10-20% above last year’s levels, with the current spot rate levels pushing shippers to conclude negotiations at the higher rates.”

Drewry said its Shipper Benchmarking Club, which allows shippers to anonymously divulge contract rates, is showing a marked year-on-year decline, though Heaney cannot divulge the amounts he said they were “definitely lower”.

Heaney said that Asia to Europe rates are normally negotiated earlier than on the Pacific and the contract discussions had all but ended before the Red Sea crisis began, so carriers could not benefit from the spike in spot rates.

Shipbroker Braemar added: that headline freight indices are not displaying a surge in spot rates right now.

“The latest surge in spot earnings, driven by Red Sea avoidance, peaked in February 2024. Since then, a gentle erosion of spot rates has been in play,” said Braemar researcher Jonathan Roach.

He added: “We would expect freight rates to remain elevated compared to pre-Red Sea avoidance at the back end of 2023. However, with the increasing weight of the heavy newbuilding program in full force, a continued but controlled softening of spot rates is expected in the short term.”

This view is, again, not mirrored by Linerlytica, who take the view that new vessel deliveries which are continuing at pace, more than 300,000 teu per month according to the analyst, will be deployed on Red Sea diversions and the additional summer service deployments, which will “continue to soak up all available supply”.

The number of ships diverted to the Cape route remains at 4.6m teu and is expected to break through the 5m teu mark in the coming weeks. “The Cape diversion continues to be the main driver behind the absorption of the active fleet,” said the analyst.

Heaney, however, said that the glut of new buildings and the existing over-capacity were offset by the initial concern as the Red Sea crisis began.

“Panic saw rates spike at the beginning of the year in what was a kind of Covid PTSD, but then the market adjusted to the new normal and saw there was sufficient surplus capacity to cope,” explained Heaney.

Where both Drewry and Linerlytica agree is that the charter rates are holding up, with the Hong Kong analyst saying charter rates are still rising for all vessel sizes apart from the smaller sectors below 1,200 teu.

Heaney confirmed that in his view the charter market was “just about holding up” but pointed out that there was normally a correlation between spot rates and charter rates, which was now out of synch.

To read it in seatrade-maritime.com: click here

RELATED STORIES

.jpg)

.jpg)

.jpg)

Water Levels Along Rhine, Danube Rivers Sink to Record Lows

Europe's Rhine River has fallen to record low l...

Know More

The Data Center Boom Has a Component Problem

Strip away the ribbon cuttings and the renderin...

Know More.jpg)

The importance of insurance during the supply chain cannot be ignored.

For decades, cargo criminals followed a familia...

Know More.jpg)

Iran Demands Crew, Cargo Details to Allow Ships Through Hormuz - SupplyChainBrain

Vessels seeking to transit the Strait of Hormuz...

Know More

Iran War Threatens Global Food Supply Chains - SupplyChainBrain

While the Iran war's impact on oil prices has c...

Know More

Maersk Adjusts Emergency Contingency Surcharges Amid Regional Disruptions - SeasNews

Maersk has announced adjustments to its Emergen...

Know More

Container rates climb after weeks of decline - Shipping Watch

The price of container freight from Shanghai to...

Know More

Trump’s Maritime Golden Age could prove costly for shipping - Seatrade-Maritime

With the USTR fees on Chinese built and owned v...

Know More

Yard Bottlenecks Ripple Through Supply Chains in 2026 - SupplyChainBrain

Once an afterthought in supply chain strategy, ...

Know More

MENA set to lead global sustainable aviation fuel market - Technical Review Middle East

The Middle East and North Africa (MENA) region ...

Know More

The New Economics of Warehousing: Flexibility Over Footprint - SupplyChainBrain

The warehousing landscape is undergoing a quiet...

Know More

Retail giants back first e-ammonia boxship - splash247

The Zero Emission Maritime Buyers Alliance (ZEM...

Know More

Shipping lines gear up for post-Red Sea crisis restructure - SeaTrade Maritime

Seatrade Maritime News and MDS Transmodal exami...

Know More

What Peak Season 2024 Taught Us About the New Rules of Holiday Shipping - SupplyChainBrain

Last year’s peak season proved what many ...

Know More

Welcome to the age of uncertainty - splash247

The opening Big Issues session of the Maritime ...

Know More

Jebel Ali Port breaks nine-year record for container volume in July on Cepa deals - The National News

DP World’s Jebel Ali Port has reported it...

Know More

Box rates rates sink to lowest levels since Red Sea crisis - Splash247

Container freight rates are sliding further, wi...

Know More

UN: Trade reset, geopolitics to hurt container trade growth - FreightWaves

Maritime trade is entering a period of fragile ...

Know More

Carriers reroute fleets to sidestep US levy - splash247

Global shipping is realigning fleets in anticip...

Know More

EU Takes Aim at Shein and Temu Over Flood of Unsafe Products - SupplyChainBrain

EU Justice Commissioner Michael McGrath is vowi...

Know More

Second half air cargo volumes depend on market diversification - Air Cargo News

Air cargo demand growth is present outside of t...

Know More

Up to Dhs500,000 fine for firms circumventing Emiratisation targets: Ministry - gulftoday.ae

The Ministry of Human Resources and Emiratisati...

Know More

Shipping in wait-and-see mode as Iran and Israel conflict continues - lloydslist.com

TANKER rates remain elevated, along with the fo...

Know More

Container freight rates fall but Red Sea return will be tipping point - seatrade-maritime.com

The Drewry World Container Index (WCI) shed a f...

Know More

AD Ports Group Opens First Inland Dry Port Facility in Abu Dhabi - transportandlogisticsme.com

AD Ports Group has announced the inaugu...

Know More

Carriers cautious on return to Red Sea as Houthis say they will end attacks - FreightWaves.com

Yemen’s Houthi rebels said they will ceas...

Know More

Have carriers failed to adjust to a new normal? - Seatrade-Maritime

Liner shipping operators are failing to act on ...

Know More

Shippers warned to ensure contingency plans are in place ahead of a potential strike at US East Coast and Gulf Coast ports next week - Container News

Transportation and logistics providers, port op...

Know More

Ships Fleeing the Red Sea Now Face Perilous African Weather - SupplyChainBrain

Ships sailing around the southern tip of Africa...

Know More

The U.S.-China Trade War Heats Up, And Businesses Move to Adjust - -SupplyChainBrain

The “quiet” trade war that has been...

Know More

More ships and more containers needed for 'feverish' box shipping sector - The Loadstar

Supply in container shipping has become “...

Know More

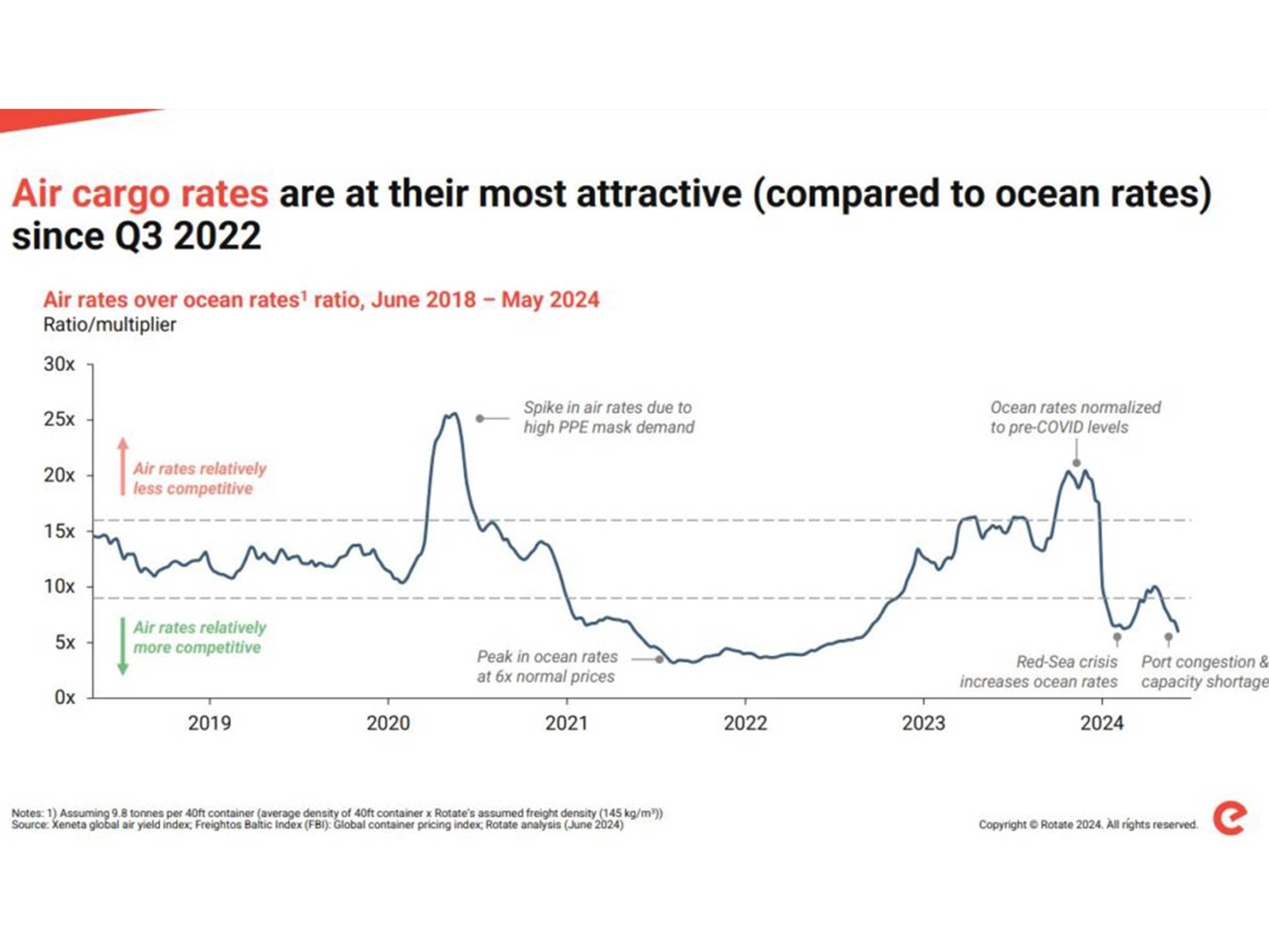

Ocean and airfreight rate differential narrows - Air Cargo News

The difference between ocean and airfreight rat...

Know More

US Demand For Goods From 2 Chinese Firms Sends Air Cargo Rates Soaring - NDTV

Two Chinese companies have turned the global ai...

Know More

Mounting container shortages creating 'total havoc' - The Loadstar

Containers out of northern China are becoming i...

Know More

11,100 new slots a day: April smashes records for liner deliveries - Splash247

The teu tsunami coming out of Asian yards shows...

Know More

Jebel Ali returns to top-10 busiest container ports - Container News

Alphaliner's report said the Middle East’...

Know More

The Evolution of Physical Security Technology in the Supply Chain Industry - SupplyChainBrain

The seamless operation of supply chains, which ...

Know More

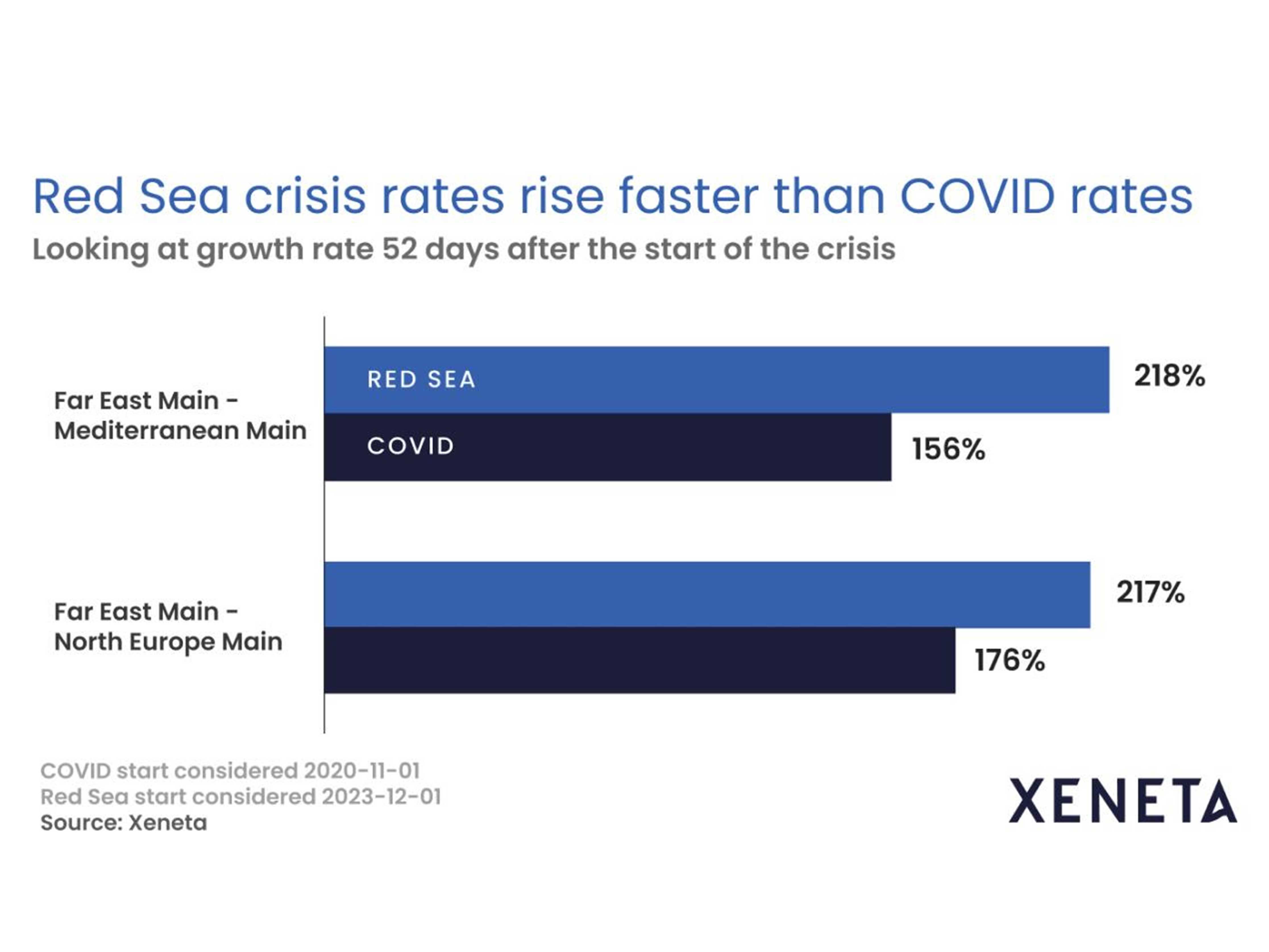

Red Sea crisis impact on box rates more rapid than Covid-19 - Asean Lines

The Red Sea crisis has seen ocean freight rates...

Know More

Freight crime on the up as gangs become more tech-savvy - The Loadstar

Internet-enabled crime and insider involvement ...

Know More

High demand, low supply: Dubai faces warehouse shortage amid new business influx - Logistics Middle East

Dubai is facing a shortage of warehouse space, ...

Know More

VGM container weight mis-declaration 'rampant at most ports', say forwarders - The Loadstar

Container carriers are dealing with widespread ...

Know More

CMA CGM announces overweight surcharge from Middle East Gulf to Europe and Mediterrannean - Container News

CMA CGM announced it will implement a new overw...

Know More

Bleak outlook for box trades as demand weakens prior to Golden Week - The Loadstar

Export bookings leading up to China’s Gol...

Know More

Ship queue grows at both ends of Panama Canal and congestion builds - The Loadstar

Draught limits on vessels seeking passage throu...

Know More

Over 60% of Logistics Companies Are Investing in Supply Chain Management Systems-SupplyChainBrain

Almost two-thirds of logistics companies (64%) ...

Know More

Growing India-UAE trade flows to benefit from domestic currency invoicing - The Loadstar

After a free trade deal last year, India and th...

Know More

Air cargo market still weakening while players search for optimism - The Loadstar

News that airlines are starting to park some fr...

Know More

Box rates to Gulf and S America rise as Asia-Europe/US prices falter - The Loadstar

Container freight rates from China to ’em...

Know MoreUp to Dh5,000 fine for owners of some vehicles who fail to register in tracking system before October 30 - Khaleej Times

The Federal Authority for Identity, Citizenship...

Know More

Plot a (positive) course for air freight rates...if you dare - The Loadstar

Amidst the economic doom and gloom, with claims...

Know More

Imports Continue Slow Climb Despite Cuts in 2023 Forecast - The Maritime Executive

The Global Port Tracker has not yet forecast th...

Know More

Some ocean trades stabilising, but transatlantic rates still falling - The Loadstar

Container spot rates from North Europe to the U...

Know More

UAE announces fees on international imports in 2023 - Arabian News

The UAE is set to introduce new import rules, s...

Know More

China's Lockdowns are Over, but its Shipping Outlook is Still Mixed- The Maritime Executive

Beijing’s on-and-off COVID lockdowns crea...

Know More

Ocean carriers plan to blank half their sailings from Asia, post-CNY - The Loadstar

Against a background of extremely weak demand f...

Know More

Airfreight loses as shippers switch to cheaper ocean routes to save costs - The Loadstar

Shippers are merrily switching modes, back to s...

Know More

Protests at China lockdowns spread, with supply chains looking vulnerable again - The Loadstar

Anti-lockdown protests have broken out across m...

Know More

Air cargo peak season evaporates on low demand, higher capacity

It’s the time of year when retailers typi...

Know More

Black Sea ro-ro operations adapt to the new normal as companies seek opportunities - The Load Star

War in Ukraine has forced the re-routing of car...

Know More

Port of Felixstowe strike could see air cargo demand rise further: Air Cargo News

Strike action at the UK’s biggest contain...

Know More

Why container ships probably won't get bigger: BBC

When the Ever Ace, one of the largest container...

Know More

Consumers Prefer Personal Touch, Predictability, Over Super-Fast Delivery

To successfully ride the bucking growth of e-co...

Know More

Air freight 'turned upside down' as capacity slumps and rates climb

Air freight capacity has indeed shrunk, accordi...

Know More

Robotics in Warehouses- Enabling smarter and more cost-efficient logistics

Warehouses are the heart of supply chains and a...

Know More

DP World reports strong volume growth of 17.1% in 2Q 2021

DP World Limited handled 19.7 million TEU (twen...

Know More

Maersk to redesign its ocean network in West & Central Asia

Maersk is redesigning its ocean network in West...

Know More

DP World acquiring Imperial Logistics for $890m expanding Africa footprint

DP World has announced an offer to acquire Sout...

Know More

Secondhand Containership Market Heats up in 2021 driven by demand

Skyrocketing container shipping freight rates a...

Know More

DP World acquires leading US-based supply chain solutions provider - GCC Ports

DP World announces the acquisition of 100 per c...

Know More

Hapag-Lloyd and ONE join Maersk’s blockchain platform

Two of the largest container carriers in the wo...

Know More

Hapag-Lloyd to provide full transparency on vessel arrivals.

With this initiative on schedule reliability, H...

Know More

Just when you think shipping costs can’t go higher, increasing fuel cost are going to push prices up for shippers.

The price of Brent crude topped $72 per barrel ...

Know More

Port of Shenzhen faces severe congestion: container-news.com

The congestion at the Port of Shenzhen, China, ...

Know More

Hapag-Lloyd further expands its container fleet: 60,000 TEU of standard containers ordered- gccports.com

The sharp increase in demand has led to a short...

Know More

Globally, container manufacturing is controlled by three companies. Here is an insight into how this is impacting the global supply chain.

Never before has the humble ocean shipping cont...

Know More

UAE to allow investors full ownership of companies from June 1 - Khaleej Times

The landmark reform was originally slated to ro...

Know More

Logistics Passport: A game-changer for Dubai trade.

The WLP will be playing an instrumental role in...

Know More

Desperate shippers swallow contract rates at double 2020 Levels - container-news.com

Early indications from the annual contract nego...

Know More

Volatility in the shipping market likely to continue till Q4 - Sea Trade Maritime News

In a trading update for Q1 2021 Maersk signific...

Know More

UAE economy performs better than expected, on track towards recovery in 2021 - Khaleej Times

The UAE economy performed better than expected ...

Know More

2020 – A year of remarkable turnaround for container shipping

Due to the change in shopper behavior during th...

Know More

2021 Trends In Retail Automation And Store Supply Chains

Some container vessels have been sailing from A...

Know More

Container shortages the biggest disrupter: where are all the empty boxes?

Some container vessels have been sailing from A...

Know More